掃碼下載APP

及時(shí)接收考試資訊及

備考信息

新用戶掃碼下載

新用戶掃碼下載安卓版本:8.8.0 蘋果版本:8.8.0

開發(fā)者:北京正保會(huì)計(jì)科技有限公司

應(yīng)用涉及權(quán)限:查看權(quán)限>

APP隱私政策:查看政策>

HD版本上線:點(diǎn)擊下載>

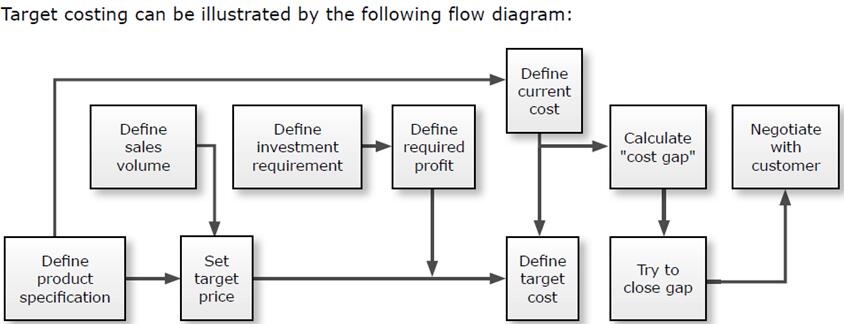

目標(biāo)成本法 Target Costing

定義:

目標(biāo)成本法是指以給定的競爭價(jià)格為基礎(chǔ),從而決定產(chǎn)品的成本,以保證實(shí)現(xiàn)預(yù)期的利潤。目標(biāo)成本法的核心工作是制定企業(yè)新產(chǎn)品的目標(biāo)成本,并不斷改進(jìn)產(chǎn)品與工序設(shè)計(jì),從而確保新產(chǎn)品的成本小于或等于目標(biāo)成本。

Target costing is an attempt to achieve an acceptable margin in a situation where the price of a product is determined externally by the market. This acceptable margin is achieved by identifying ways to reduce the costs of producing the product.

目標(biāo)成本法的步驟:

1. 通過研究市場,確定產(chǎn)品的市場接受度,考慮市場份額;

Determine the price the market will accept for the product, based on market research. This may take into account the market share required.

2. 從價(jià)格中扣除必要的利潤率,以得到目標(biāo)成本;

Deduct a required profit margin from this price—this gives the target cost.

3. 預(yù)估產(chǎn)品的實(shí)際成本。如果是一個(gè)新產(chǎn)品,預(yù)估成本將是一個(gè)估價(jià);

Estimate the actual cost of the product. If it is a new product, this will be an estimate.

4. 設(shè)法縮小產(chǎn)品的實(shí)際成本和目標(biāo)成本差距 。

Identify ways to narrow the gap between the actual cost of the product and the target cost.

歷年樣卷

考試大綱

詞匯表

報(bào)考指南

考官文章

思維導(dǎo)圖

新用戶掃碼下載

新用戶掃碼下載安卓版本:8.8.0 蘋果版本:8.8.0

開發(fā)者:北京正保會(huì)計(jì)科技有限公司

應(yīng)用涉及權(quán)限:查看權(quán)限>

APP隱私政策:查看政策>

HD版本上線:點(diǎn)擊下載>

官方公眾號

微信掃一掃

官方視頻號

微信掃一掃

官方抖音號

抖音掃一掃

Copyright © 2000 - m.electedteal.com All Rights Reserved. 北京正保會(huì)計(jì)科技有限公司 版權(quán)所有

京B2-20200959 京ICP備20012371號-7 出版物經(jīng)營許可證 ![]() 京公網(wǎng)安備 11010802044457號

京公網(wǎng)安備 11010802044457號

套餐D大額券

¥

去使用 主站蜘蛛池模板: 国产一区二区三区免费 | 国产成人精品一区二区 | 亚洲国产一区二区在线 | 精品国产精品 | 玖玖国产精品视频 | av片在线免费观看 | 久久精品视频偷拍 | 天堂网www| 在线小视频 | 欧美精品一区在线观看 | 国产一区二区毛片 | 欧美性天天影院 | 成人手机视频在线 | 国产成人精品一区二区三区视频 | 国产一区二区高清视频 | 午夜精品久久久久久久久久久久久 | 九九九九精品 | 亚洲一区二区三区在线免费观看 | 日韩精品影视 | 久久免费中文视频 | 国产精品久久久久久久免费软件 | 精品久久久久久 | 国内av免费 | 日韩精品在线视频 | 黑人av| 男人天堂av网站 | 62久久久成人精品电影 | 亚洲一区h | 女人18毛片九区毛片在线 | 日韩日日日 | 97国产在线视频 | 一区二区自拍 | 色综合久久88色综合天天 | 日韩毛片在线看 | 国产精品久久久久久久久 | 久久久久一区 | 99re在线播放视频 | 精品视频久久久久久 | 欧美国产高清 | 国产福利在线看 | 在线射 |